A merchant account is a specialized type of business bank account that enables businesses to accept various forms of electronic payments, most commonly debit and credit cards. When a customer makes a purchase, their payment is processed and temporarily held in the merchant account before being transferred to the business’s bank account. Essentially, the merchant account acts as an intermediary between the customer’s payment method and the business, ensuring the smooth transfer of funds.

For businesses of all sizes, whether operating in physical stores or online, having a merchant account is essential for processing transactions in a fast, secure, and reliable manner. Without one, businesses would be limited to accepting cash, checks, or slower traditional methods of payment, which could significantly reduce their ability to compete in today’s fast-paced, digital economy.

Importance of a Merchant Account for Businesses

Merchant accounts are critical for businesses as they facilitate efficient and secure payment processing, which is vital for building trust with customers and increasing sales. Here’s why merchant accounts are so important:

- Payment Flexibility: They allow businesses to accept multiple forms of payment, such as credit and debit cards, contactless payments, and mobile wallets (e.g., Apple Pay and Google Pay). This versatility is key to offering customers convenient payment options.

- Global Reach: Merchant accounts enable businesses to accept payments from customers all over the world, making it easier to expand into international markets.

- Transaction Security: Merchant accounts provide robust security features that protect both businesses and customers from fraud, chargebacks, and unauthorized transactions.

- Faster Payments: These accounts speed up the payment process, reducing the time it takes for funds to reach a business’s bank account, thus improving cash flow.

- Professional Image: Businesses with merchant accounts look more professional, as they can offer secure and modern payment solutions. This helps instill confidence in customers and enhances brand credibility.

2. What is a Merchant Account?

Detailed Explanation of a Merchant Account

A merchant account serves as a bridge between a business, its customers, and the financial institutions that process payments. When a customer makes a purchase using a debit or credit card, the funds don’t go directly from the customer’s card to the business’s bank account. Instead, the transaction passes through several stages:

- Authorization: The customer’s bank checks whether there are sufficient funds or credit to complete the transaction. Once authorized, the transaction is approved.

- Capture: The amount is “captured” from the customer’s account and held in the merchant account.

- Settlement: The funds are then settled between the customer’s bank and the merchant’s acquiring bank.

- Funding: The money is transferred from the merchant account to the business’s bank account, typically within 1 to 3 business days.

This multi-step process ensures that both the customer and the business are protected from fraud and that the transaction is processed securely.

Merchant Account vs. Payment Gateway

While a merchant account and a payment gateway both play a role in processing payments, they serve different functions:

- Merchant Account: This is the business’s bank account where funds from credit card transactions are held before they are deposited into the business’s regular bank account.

- Payment Gateway: The payment gateway is the technology that encrypts and securely transmits transaction data between the merchant’s website (or point-of-sale system) and the acquiring bank. In other words, the payment gateway acts as the digital “gatekeeper” that approves or declines transactions and ensures data security during the process.

For an online business, both a merchant account and a payment gateway are needed to complete card transactions. A common misunderstanding is that the gateway is the merchant account itself, but it’s more like the “connector” or “processor” for those payments.

Is a Merchant Account the Same as a Bank Account?

No, a merchant account is not the same as a traditional bank account. Although they are both financial accounts used by businesses, they serve very different purposes:

- Merchant Account: Specifically used for receiving funds from credit and debit card transactions, and it’s temporarily held here before transferring to the business’s regular bank account.

- Business Bank Account: A typical business checking or savings account where businesses manage their cash flow, pay bills, and deposit revenue.

Unlike a regular bank account, a merchant account often comes with transaction fees, setup costs, and monthly charges, as it provides additional services like fraud prevention, customer support, and compliance with payment industry regulations.

3. Types of Merchant Accounts

Retail Merchant Accounts

Retail merchant accounts are designed for businesses that operate in physical, brick-and-mortar locations. These accounts allow merchants to process in-store payments using credit card terminals, point-of-sale (POS) systems, or mobile card readers. Retail merchant accounts are ideal for businesses like restaurants, boutiques, and grocery stores, where customers typically present their cards in person to complete transactions.

- Key Features: In-person transactions, fast approvals, lower transaction fees (compared to online accounts), support for various payment types (cards, mobile wallets).

E-Commerce Merchant Accounts

E-commerce merchant accounts cater to businesses that operate online, allowing them to accept payments from customers through their websites or apps. These accounts are essential for online retailers, subscription-based services, and digital marketplaces. With an e-commerce merchant account, businesses can accept payments from around the globe, and the account integrates seamlessly with payment gateways to ensure secure, encrypted transactions.

- Key Features: Secure payment processing, global reach, integration with payment gateways, support for multiple currencies, higher security due to the absence of physical card use.

Mobile Merchant Accounts

As more businesses operate on-the-go, mobile merchant accounts have become increasingly popular. These accounts are ideal for businesses that sell products or services outside of a traditional store, such as food trucks, event vendors, or service professionals like plumbers and electricians. With a mobile merchant account, businesses can use mobile card readers that connect to smartphones or tablets to process payments.

- Key Features: Portable card readers, ability to process payments from anywhere, mobile app integration, on-the-spot payment capability.

High-Risk Merchant Accounts

Some businesses fall into the “high-risk” category due to the nature of their industry, transaction volume, or potential for chargebacks. Industries like online gambling, adult services, telemarketing, and subscription services are considered high-risk because they experience higher instances of fraud and chargebacks. High-risk merchant accounts come with higher fees and stricter terms to mitigate the risks for payment processors.

- Key Features: Higher transaction fees, stringent compliance requirements, risk management tools, additional fraud prevention measures.

4. Merchant Account Providers: Examples and Comparison

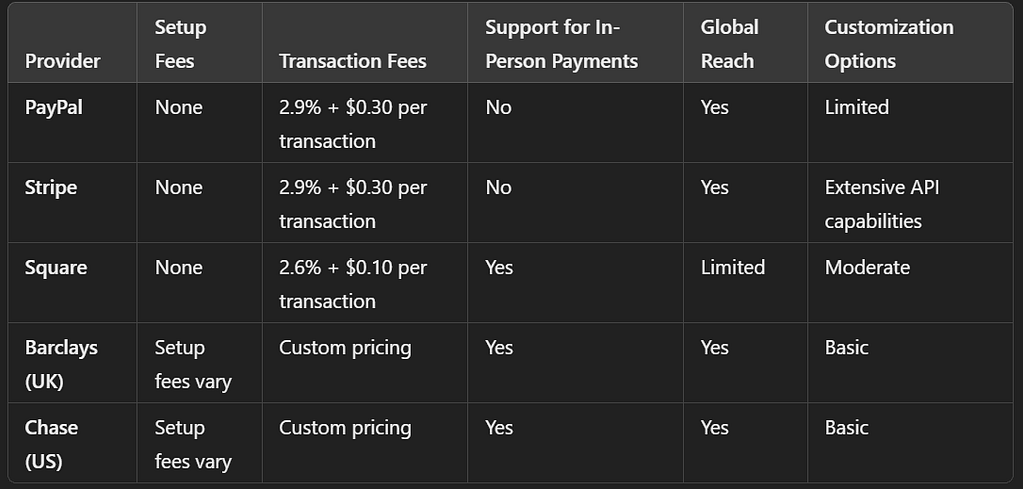

Examples of Merchant Account Providers

Merchant account providers play a pivotal role in helping businesses process payments securely and efficiently. Below are some prominent examples of providers, each with unique features catering to different business needs.

- PayPal:

Is PayPal a merchant account? The answer is yes and no. PayPal functions as a payment aggregator rather than a traditional merchant account. While it allows businesses to accept payments from customers, the funds first go into PayPal’s central merchant account before being transferred to the business. It provides ease of use, no setup fees, and flexibility, making it suitable for small businesses or freelancers. However, it may not be ideal for large-scale businesses that require more direct control over funds.- Key Features: Instant setup, global payment acceptance, multi-currency support, but with relatively higher transaction fees and limited control over the payment process.

- Stripe:

Is Stripe a merchant account? Yes, but it’s much more than just a merchant account provider. Stripe offers a complete suite of developer tools, making it highly customizable for businesses seeking advanced payment solutions. Unlike PayPal, Stripe allows businesses to integrate payments directly into their websites or apps using APIs, making it ideal for tech-savvy businesses that need flexibility. Stripe is popular with startups, tech firms, and larger enterprises due to its scalability and robust infrastructure.- Key Features: Custom integrations, recurring billing, global reach, and support for over 135 currencies, with transparent pricing.

- Square:

Square has revolutionized payment processing, especially for small businesses and mobile merchants. It provides a seamless solution for both in-person and online payments. Square’s hardware (like card readers and POS systems) is popular among retail businesses, cafes, and service professionals. In addition to its physical point-of-sale hardware, Square offers an integrated eCommerce solution that makes it easy for businesses to sell online.- Key Features: Versatile hardware, mobile payments, no monthly fees for basic plans, and simplified pricing with a flat-rate structure.

- Traditional Bank Merchant Accounts:

Many traditional banks, especially large ones, offer merchant account services to businesses. Examples from major UK and US banks include Barclays, HSBC, Lloyds (UK), and Chase, Bank of America, Wells Fargo (US). These banks provide tailored solutions with a long-standing reputation for trust and reliability. However, they often come with more complex setups, higher fees, and less flexibility than modern payment solutions like Stripe or Square.- Key Features: Trusted financial institutions, full-service business banking options, but with higher upfront costs, monthly fees, and more extensive paperwork.

Comparison Table of Key Providers

Here’s a side-by-side comparison of some key features, fees, and benefits of popular merchant account providers:

This comparison helps businesses select the right provider based on factors like cost, ease of setup, and the types of payments they need to accept.

5. How Does a Merchant Account Work?

Step-by-Step Breakdown of a Transaction

A merchant account works behind the scenes every time a customer makes a payment. Here’s a step-by-step breakdown of how the process unfolds:

- Customer Initiates a Payment:

The customer swipes their card, taps their mobile wallet, or enters their payment details online to make a purchase. - Authorization:

The payment information is transmitted to the payment gateway (e.g., Stripe, PayPal), which encrypts the data and forwards it to the acquiring bank (the merchant’s bank). The acquiring bank then sends a request to the customer’s issuing bank (the bank that issued the card). - Approval/Denial:

The customer’s bank verifies the payment details, checking for available funds or credit. If everything checks out, the payment is authorized, and the transaction moves to the next step. - Capture:

Once the payment is authorized, the funds are “captured” by the merchant account. This amount is now reserved for the merchant, awaiting final settlement. - Settlement:

The acquiring bank (the merchant’s bank) settles the transaction by transferring the funds from the customer’s bank to the merchant account. - Funding:

Finally, the funds held in the merchant account are transferred to the business’s regular bank account, typically within 1 to 3 business days.

Merchant Account Fees

Merchant accounts come with a variety of fees, which can vary depending on the provider and the type of transactions being processed. Here are some common fees associated with merchant accounts:

- Transaction Fees: A percentage of each transaction, typically ranging from 1.5% to 3.5% for credit card transactions. Fees may also include a fixed amount per transaction.

- Setup Fees: Some providers charge a one-time setup fee to create the merchant account and integrate payment systems.

- Monthly Fees: These fees cover ongoing account maintenance, technical support, and other services.

- Chargeback Fees: In cases of disputed transactions, merchants may be charged a fee for handling chargebacks.

- Cross-Border Fees: For international transactions, some providers charge additional fees for currency conversion and cross-border processing.

These fees exist because processing payments involves risk (such as fraud), infrastructure, and technology costs for both the merchant account provider and the payment processors.

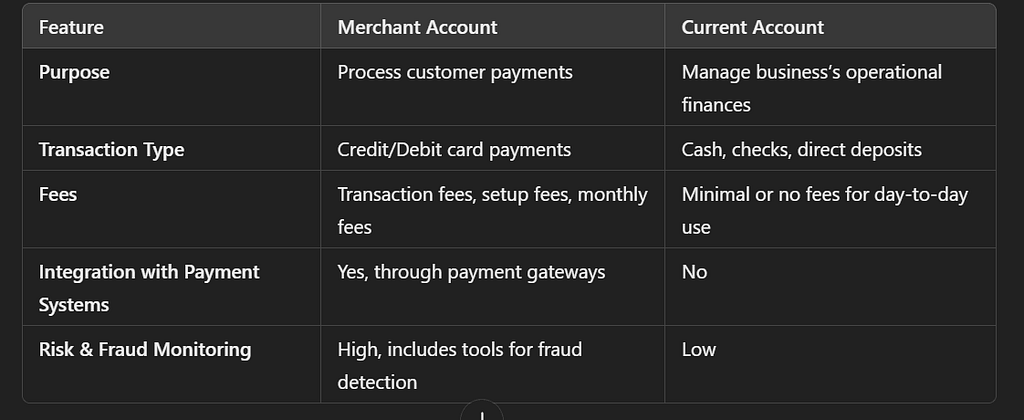

6. Merchant Account vs. Current Account

Differences Between Merchant Accounts and Current Accounts

While both merchant accounts and current accounts are essential to business operations, they serve very different purposes.

- Merchant Account:

A merchant account is solely used for handling payments made by customers using credit or debit cards. Its primary function is to act as a holding account where transaction funds are processed before being transferred to the business’s regular bank account. Merchant accounts come with special features like fraud detection, chargeback handling, and integration with payment gateways. - Current Account:

A current account (also known as a checking account in the US) is a standard business account used for day-to-day operations, such as paying suppliers, handling payroll, and managing cash flow. It does not handle credit card processing or payment settlement but is essential for the regular functioning of a business.

By understanding the differences between these account types, businesses can ensure they are using the right financial tools for their payment and operational needs.

7. Merchant Accounts for Small Businesses

Why Small Businesses Need Merchant Accounts

For small businesses, a merchant account can be a game-changer. It allows businesses to accept a variety of payment methods, particularly credit and debit cards, which are the most popular forms of payment globally. Accepting card payments not only provides convenience to customers but also helps build trust and credibility, making your business appear more professional. Moreover, having a merchant account enables small businesses to expand their customer base by offering online payment options, which is crucial in today’s eCommerce-driven world.

By streamlining the payment process, merchant accounts can improve cash flow management, reduce the risk of unpaid invoices, and provide real-time access to sales data. They also enhance the customer experience, as consumers are increasingly expecting fast, secure, and versatile payment options.

- Growth Potential: Small businesses can experience significant growth by offering customers flexible payment methods.

- Professionalization: Accepting card payments gives a business an air of legitimacy, as many customers expect modern payment options.

Affordable Options for Small Businesses

While traditional merchant accounts might come with steep fees, several providers offer affordable solutions specifically designed for small businesses. These include low-fee or no-monthly-fee options, making it easier for small enterprises to start accepting payments without breaking the bank.

- Square: Known for its ease of use, Square offers free hardware (like card readers) and no monthly fees for basic plans. Small businesses only pay per transaction, making it ideal for businesses with variable sales volumes.

- PayPal: PayPal provides a cost-effective solution for small businesses that want to start accepting payments quickly. It has no monthly fees and only charges transaction fees, making it a great option for businesses with lower sales volumes.

- Stripe: Stripe offers a slightly more advanced platform, particularly for small online businesses. With no setup fees and only per-transaction charges, Stripe is highly scalable for small enterprises that plan to grow over time.

Other providers to consider include Square, SumUp, Clover, and Helcim, which all provide tailored solutions for small businesses with flexible pricing plans.

8. How to Open a Merchant Account

Merchant Account Opening Process

Opening a merchant account involves several key steps that require documentation, assessment, and approval by the merchant service provider. Here’s a step-by-step guide to help small businesses through the process:

- Choose a Merchant Account Provider:

Start by comparing different providers based on their fees, services, and features. It’s essential to choose one that aligns with your business size and payment needs. - Application Submission:

Once you’ve selected a provider, you’ll need to submit an application. This typically includes business information like your business name, address, tax ID, banking details, and estimated monthly transaction volume. - Documentation Required:

Providers will usually ask for certain documents, including your business license, bank statements, tax returns, and financial statements. If you operate a high-risk business, you may need to provide additional information. - Underwriting Process:

The provider’s underwriting team will review your application to assess your business’s risk level. This process helps determine the fees you’ll pay and whether your application will be approved. - Approval and Setup:

Once approved, the provider will set up your merchant account, which may include connecting it to your payment gateway or point-of-sale system. The entire process usually takes 1-2 weeks, although some providers offer faster setups.

What to Look for When Opening a Merchant Account

Choosing the right merchant account provider depends on several factors, including:

- Transaction Volume: If your business processes many small transactions, look for a provider that offers lower per-transaction fees.

- Risk Category: High-risk businesses, such as those in adult services or gaming, should look for specialized providers experienced in handling high-risk merchant accounts.

- Business Needs: Consider whether you need eCommerce support, mobile payments, or POS systems. Providers like Square and Stripe offer tailored solutions based on these needs.

- Fees and Contracts: Pay attention to the fee structure. Some providers charge monthly fees, transaction fees, or additional fees for chargebacks. Opt for a transparent pricing model that suits your budget.

9. Common FAQs on Merchant Accounts

1. What is a Merchant Account in Banking?

A merchant account is a specific type of bank account that allows businesses to accept and process payments, primarily from credit and debit cards. It acts as an intermediary between the customer’s bank and the business’s bank, ensuring that funds are transferred securely after a transaction is made.

2. Is a Merchant Account Required for eCommerce?

Yes, most eCommerce businesses need a merchant account to process online payments. However, alternatives exist, such as payment aggregators (e.g., PayPal, Stripe), which allow businesses to accept payments without opening a dedicated merchant account.

3. What is a Merchant Account Scanner?

A merchant account scanner, also known as a card reader, is a device used to read card information during in-person transactions. These scanners are essential for brick-and-mortar businesses and are often part of a point-of-sale (POS) system.

4. Can You Get a Merchant Account Without a Business?

Generally, no. Merchant accounts are designed specifically for business use, and banks require documentation proving that you’re operating a legitimate business. However, individual sellers or freelancers can often use services like PayPal, which function as payment aggregators.

5. Are Merchant Account Fees Negotiable?

In some cases, yes. High-volume businesses may be able to negotiate lower transaction fees with their merchant account providers. It’s always a good idea to discuss fee structures upfront and see if discounts are available based on your business type and transaction volume.

10. Merchant Account Scanners and Hardware

Devices that Support Merchant Accounts

To process in-person payments, businesses need hardware that supports merchant accounts. The most common devices include:

- Point-of-Sale (POS) Systems:

These are all-in-one systems that include card readers, receipt printers, and cash drawers. POS systems like Square POS and Clover are popular among retailers and restaurants. - Mobile Card Readers:

These portable devices connect to smartphones or tablets to process payments on the go. They are particularly useful for small businesses or service providers who operate outside of a traditional storefront. Devices like the Square Reader and PayPal Here are commonly used in this space. - Contactless Payment Terminals:

As contactless payments become more popular, businesses can use terminals that accept payments via NFC (Near Field Communication), enabling customers to pay using mobile wallets like Apple Pay or Google Pay.

Having the right hardware ensures seamless transaction processing and enhances the customer experience, especially for businesses with a physical location.

11. Conclusion

Key Takeaways

Merchant accounts are an essential tool for businesses of all sizes, enabling them to process payments securely and efficiently. Whether you run an eCommerce store, a brick-and-mortar shop, or operate in a high-risk industry, there’s a merchant account solution tailored to your needs. The key is to choose a provider that aligns with your transaction volume, business type, and risk category. Additionally, understanding the fees associated with merchant accounts is crucial for managing costs effectively.

{kind=link}